Many retirees with a steady income from their 401(k) or traditional IRA accounts may have never considered a Roth conversion strategy. Other retirees might have looked at a Roth conversion in the past but thought it might not be for them because paying the required taxes up front can be a tough pill to swallow.

However, for married couples entering retirement, evaluating Roth conversions is a worthwhile endeavor. If one spouse dies before the other and the surviving spouse does not remarry, the surviving spouse may face much higher tax rates than if the deaths are contemporaneous.

This can occur because:

Let’s evaluate a hypothetical retired couple, Mr. and Mrs. Frugal.

They are both 71 years old, live in California, and expect to spend about $100,000 this year. They anticipate their spending will grow 2.5% per year. Although their financial advisor informed them that moving to another state would likely reduce both their taxes and living expenses, they have family here and do not wish to move. They do not expect tax brackets to adjust except for inflation (they expect the Tax Cuts and Jobs Act will be renewed).

Although they were aggressive investors, they became more conservative as they approached retirement. They have a $20,000,000 Traditional IRA account. They only expect a 3% net annual return from the investments in their Traditional IRA accounts and 3% net tax-free municipal bond income from their brokerage account.

Despite this long list of assumptions, important financial planning information is omitted to keep this case study as simple as possible (e.g. projected Social Security benefits). Normally, we might assume a higher expected return for the IRA and Roth accounts than for the taxable account. However, we want to demonstrate that the case for Roth conversions does not rest on this assumption alone.

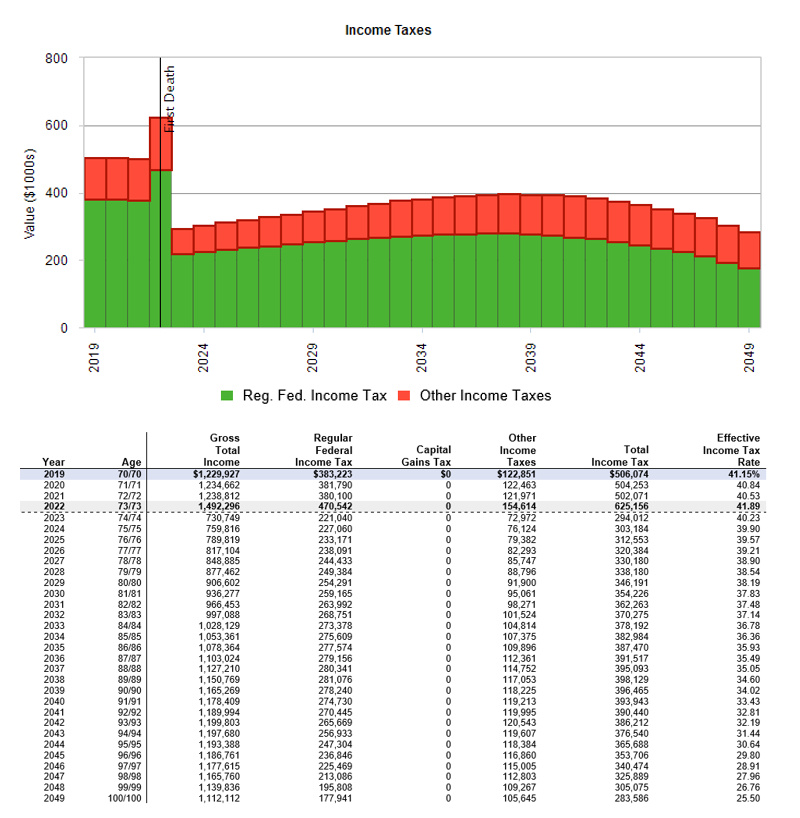

If they both live until 100 and remain married, their projected tax rates are steady for the first 15 years of their retirement before gradually declining. At first glance, this suggests little value in accelerating their income through Roth conversions, which are most beneficial when the current tax rate is lower than the projected future rate.

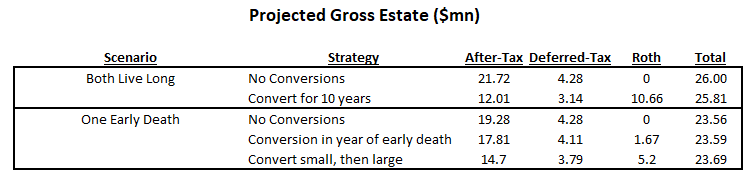

Their projected gross estate includes $21.72mn of after-tax assets and $4.28mn of deferred assets. This estate may be subject to estate tax depending on the future level of the exemption. In addition, their heirs will need to take required minimum distributions from the deferred assets. These distributions will increase their heirs’ taxable income. Note that these issues may not apply to the couple if they plan to leave their estate to charity.

Unfortunately, one spouse often outlives the other.

If Mr. Frugal dies three years from now and Mrs. Frugal does not remarry, there are significant tax implications. Mrs. Frugal’s effective tax rate is projected to increase almost 6% in the year following Mr. Frugal’s death. The after-tax assets in Mrs. Frugal’s projected estate shrink from about $21.72mn to $19.28mn –an 11% drop! Her projected IRA assets ($4.28mn) do not change as her spending is less than her required minimum distributions and the required minimum distributions do not change as a result of a spouse’s death if the spouses are the same age. This scenario reduces the amount available to give whether they plan to give to charity or to heirs.

A tax hike is not a necessary condition for an increase in a retiree’s effective tax rate!

In the year of the first spouse’s death, the surviving spouse is still able to use married filing jointly status. This gives the spouse a final opportunity to use the married brackets for withdrawals and Roth conversions from deferred tax accounts such as an IRA. Converting in the year of a spouse’s death may help reduce lifetime income taxes by reducing taxable income in future years when the survivor will likely file as single.

The surviving spouse may find it difficult to think about the future and make decisions in the year of their loved one’s death. This strategy would be especially difficult if the death is unexpected and/or occurs near the end of the year. Financial planning before the death occurs may help mitigate this stress.

This strategy has an insignificant impact on the total projected gross estate relative to doing nothing in the year of death.

However, the composition of the estate changes. Although the heirs would receive less after-tax and deferred-tax assets than if she does not do a conversion, any heirs would receive a $1.67mn Roth account, which allows for tax free growth and withdrawals.

If the couple decides to do Roth conversions each year for the next 10 years, they may not see much benefit if they both live to 100.

The couple’s projected total gross estate shrinks from $26mn to $25.81mn but includes $10.66mn of Roth assets. If they leave the estate to charity, this is a slightly worse outcome. Depending on the future estate tax exemption and the income tax rates applied to their heirs, this may be a better for the heirs than if they had done nothing.

If an early death occurs, the couple may benefit in a couple ways from doing conversions while both are still alive. First, the income from the distributions is taxed using the joint tax brackets and reduces the future required minimum distributions. Second, if the couple has done conversions in the past, the surviving spouse may be more ready and willing to do a large conversion in the year of their spouse’s death.

If the couple begins doing conversions now and the surviving spouse does a larger one in the year of first death, the projected total gross estate is $23.69mn, slightly larger than if an early death occurs and the couple does nothing. In addition, the estate includes $5.2mn of Roth assets.

Each family’s situation is unique. Without meeting with Mr. and Mrs. Frugal, we cannot say whether Roth conversions would be good for them. The answer depends on their goals, health, and family situation. If you have questions or would like us to help you evaluate if Roth conversions may be right for you, please call us today at 925-300-3222 or contact us using the form below.

This commentary reflects the personal opinions, viewpoints and analyses of the Integrity Wealth Partners, LLC employees providing such comments, and should not be regarded as a description of advisory services provided by Integrity Wealth Partners, LLC or performance returns of any Integrity Wealth Partners, LLC client. The views reflected in the commentary are subject to change at any time without notice. Nothing in this commentary constitutes investment advice, performance data, or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Integrity Wealth Partners, LLC manages its clients' accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.